Table of Content

So, there is a good chance that you may be paying a higher EMI just because your loan is not from a competitive lender. If you have not compared your interest rate, then it is a high time that you do so and check if your lender is charging a higher rate even under EBR. Since most of the home loans are on floating rate basis and there is no penalty on shifting your loan, therefore the only cost involved will be the fee charged by new lender.

As we know, a higher outstanding loan amount will attract a higher rate of interest. When borrowers use lump-sum amounts to make a prepayment for one time of home loan before the tenure ends, it is called a lump-sum prepayment. It may be the amount received as a bonus, the maturity of the borrower’s old investments, or the amount received as a gift, etc. When a borrower prepays the amount of his regular EMIs in advance, it is called the “Prepayment of the loan”. This option of prepayment is ideal for both new as well as existing borrowers as it can reduce their EMIs and interest rates.

The fourth major bank launches a program of small loans

This can be done only if short-term investments in corporate bonds do not go beyond 20% of the FPI’s total investment in such bonds. If you’re already a customer with a certain bank, it would be a wise option to consider the same bank for purchasing a loan. This could work in your favor if you have a good standing with your bank, in which case they may be very likely to provide you with a lower rate of interest on your preferred loan. If a borrower has taken the home loan at a higher interest rate, there is an option through which they can refinance their home loan by changing the home loan lender. Contributing the maximum amount from your pocket will increase the chances of loan approval. However, it is not advisable to not overstretch your finances just to pay the maximum amount.

If you had taken a fixed rate loan the chances are that you may be paying a much higher interest rate throughout your loan tenure. For instance, 5 years ago, if the floating rate loan was available at 9% interest, fixed rate loans come with interest rates of around 10.5%. And if the borrower opted for a fixed rate loan, he would be at a disadvantage in the current situation.

Don’t Skip Payments

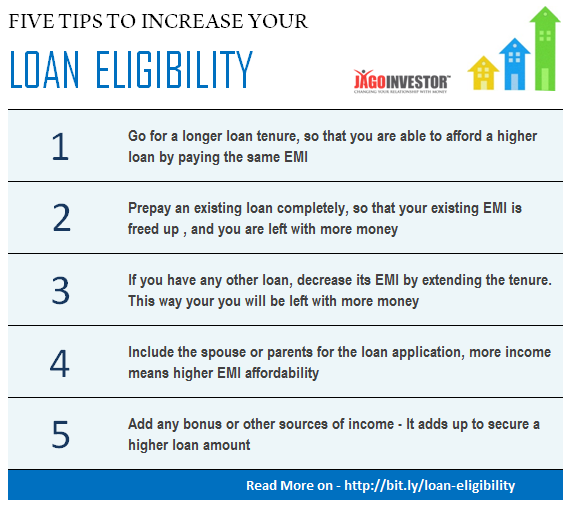

Let’s understand them collectively and see how different borrowers can reduce their EMIs, and interest rates. Here are some ways how a new or an existing home loan borrower can reduce the EMI burden of their home loan efficiently. If you encounter financial stress and wish to seek relief by lowering your Home Loan EMI, then you might as well consider extending the Home Loan tenor.

In other words, the EMIs you pay towards loan repayment stretch over a long period of time, which makes it crucial that the EMI amount is comfortable to bear, considering your income and expenses. A single default is enough to bring your credit score down by at least points. In case there is a break in your income, then you could approach the lender and request an EMI-free period. Banks do offer a waiver of three to six months on EMI payments if you’re in between jobs or your business operations have been held up.

How to Calculate The Total Cost of Buying A Flat in Bangalore

Due to this, most home loan borrowers are always on the lookout for ways to reduce their equated monthly instalment outgo. Let’s say you had availed of a fixed-rate Home Loan, the chances are higher that you are paying a higher Home Loan interest rate and will continue to do so all through your loan tenor. Lenders generally charge at least a 1-2% higher rate on fixed-rate Home Loans. Lenders finance up to 75–90% of the property’s value, leaving the balance 10–25% for you to service by means of a down payment. While you must bear this amount, it is always a good idea to see if you can pay more.

Highlight the fact that you have been a loyal customer of the bank for the past several years with a consistent history of transactions. You could also mention that other banks have offered lower interest rates for the same loan and hence seek a loan transfer. And conclude by requesting them to lower the interest rate since other banks are offering you X% interest while you’re paying Y% here. The above-mentioned points have covered everything you need to know about lowering your home loan interest rates.

Besides that, he is passionate about fitness and works hard to maintain a healthy lifestyle. It is a good option for those who are not able to make all the prepayment at once. If you have already taken a home loan and are looking to reduce your interest rates and EMIs, here are some strategies that can be adopted to reduce the EMIs and interest rates.

Only if your total loan amount (inclusive of all the charges, taxes, fees, etc.) is less than your existing lender, opt for ahome loan balance transfer. In the example above, by switching to a variable rate loan, the borrower will save Rs 4,869 per month on EMI and Rs 5.85 lakh on interest payment for the remaining term. If you have decided to take a loan and your existing bank is not offering the best deal, feel free to look around.

You should try to make at least one or two partial payments in a financial year. The partial payment will help in reaching the principal amount faster and lower the financial burden. On the other hand, if you go for Repo Linked Lending Rate linked loan from PNB then you can get a loan at a much lower interest rate as the bank's RLLR is 6.80%. Therefore, by shifting interest rate regimes, your interest rate reduces by 0.5%. A large segment of existing home loan borrowers gets so busy with their lives that after repayment starts, they often forget to check how the composition of their EMI is changing. A Home Loan is a sizeable loan with an extended repayment tenor of up to 30 years.

Based on your existing relationship with your lender and your repayment track record, you can request for a lower Home Loan interest rate. This would imply a direct EMI reduction, so much so that you could later find out how to reduce Home Loan tenor and still stay on budget. When the interest rate drops, customers who have availed floating rate of home loan will invariably pay EMI at the reduced rate of interest.

You can also check your home loan EMI for different loan amounts with the help of the calculator. Under the overdraft option, a savings or current account is opened for the home loan borrower to deposit his/her surpluses and is linked to the home loan account. The interest cost of the home loan is calculated after deducting the balance maintained in the savings/current account from the outstanding loan amount. He/she is free to withdraw from the savings/current account as and when any fund requirement arises. Lately, they have passed on the entire rate hike to customers, amid a rise in borrowing costs. All you have to do is find another lender that offers interest rates that suit your requirements and also check for other charges that they would levy.

Therefore, a borrower who is 45 years old may not get the option to extend the tenor beyond 15 years. When you avail of a housing loan, you have the choice to opt for a long tenor to make your EMIs small. However, to avoid overpaying, assess if you can manage slightly larger EMIs. The idea is that a smaller tenor implies a lower net interest payment, though it increases your EMI amount.

No comments:

Post a Comment